Source: Bain &

Company

The Private

Equity industry has grown and morphed over the nearly seven decades of its

formal existence. From primarily Venture

Capital-related funds at the outset, to Buyout strategies (and a levered

sub-segment); Secondaries; Fund of Funds; Distressed, Infrastructure; and Real

Estate, private equity has typically taken on the dynamics of the macro

environment around it, reacting to interest rate levels, spreads and the tax

code to take advantage of conditions as they have presented themselves. In this note, we will look at the development

of the industry and its major sub-segments over time and also provide our

insight as to what we think the years ahead might look like.

Background

The current view

of what constitutes the private equity industry today most likely began to take

shape in the late 1940’s when organized, professional management firms with the

sole purpose of funding private companies were established. However, for decades before this, private market

transactions were not at all uncommon.

The first major U.S. transaction was the notable buyout of the Carnegie Steel Company in 1901 by J.P.

Morgan & Company for $480 million. After

the deal closed, J.P. Morgan famously quoted,

“Congratulations Mr. Carnegie, you are the richest man in the world”, a fact of

which Andrew Carnegie was supposedly embarrassed. At the time, the $480 million transaction

value equated to over 2% of US GDP.

Today, a similarly sized transaction would have to weigh in at nearly $355

billion.

Private

acquisition activity continued apace until the early 1930’s when the Glass

Steagal Act (technically the Banking Act of 1933) forced a separation of the

activities of commercial and investment banks and hampered the further

development of the US merchant banking industry. The act essentially left private acquisition

activity as the preserve of wealthy individuals and families.

After World War

II, what are widely considered the first two modern venture capital firms were

formed. In 1946, American Research and

Development Corporation was founded by Georges Doriot with the goal of

encouraging investment in businesses run by returning soldiers. In the same year, J.H. Whitney & Company

was founded by John Hay “Jock” Whitney to provide capital and services to small

and mid-market growth companies. Based

in New Canaan, CT, J.H. Whitney & Company is still in business today.

In 1958, the

Small Business Investment Act was passed which aided in the financing and

management of smaller enterprises.

Specifically, this act provided certain firms access to federal funds

which could be levered at a rate of 4:1 against privately raised investment monies. Though helpful, the industry still remained

on the fringes of most investors’ radar.

Beginning in the

1960’s and continuing through the 70’s, the foundation upon which today’s

industry is based was laid. In the

1960’s private equity activity was predominantly centered around venture

capital firms who focused on providing funding to start and expand companies,

many of whom were in technology-related fields.

It was also during this period that the current Limited Partnership

structure for private equity funds was introduced:

- Limited Partners putting up the

money

- General Partners identifying and

acquiring investments and running the day-to-day business

- A compensation structure comprised

of a management fee plus a percentage of the profits

In 1973, the National

Venture Capital Association was founded to serve as the industry’s trade

group. However, the stock market crash

of the time quickly put a damper on fund raising and it wasn’t until 1978 that asset

gathering normalized.

Buyouts are now the

largest segment within the private equity world, with the leveraged sub-segment

often commanding much of the attention. The

first generally acknowledged leveraged buyouts were the acquisitions of

Pan-Atlantic Steamship Company and Waterman Steamship Corporation in 1955 by

McLean Industries. McLean borrowed $42

million and raised $7 million through the issuance of preferred stock. Upon closure of the deal, McLean used $20

million of the target’s cash and assets to retire some of the borrowings. This deal became a blueprint for many of the

leveraged buyouts of the 1980’s and later.

In the mid-1960’s,

Henry Kravis, Jerome Kohlberg and George Roberts, then employees of Bear

Stearns, began targeting the acquisition of family businesses that were facing

succession issues. These companies were

generally too small to take public and their founders did not care to sell out

to competitors. It wasn’t until 1976

that Kohlberg, Kravis and Roberts left Bear Stearns to form what we know today

as KKR. About the same time (1974),

Thomas H. Lee founded a new investment firm bearing his name to focus on

acquiring more mature companies in leveraged buyouts. Both firms have gone on to great successes.

The passage of

the Employee Retirement Income Security Act of 1974 (ERISA) initially stunted

industry growth as corporate pension funds were prohibited from owning what were

deemed to be “risky” investments in private companies. Largely as a result, industry-wide fund

raising fell to $10 million in 1975. In

1978, restrictions were relaxed and fund raising climbed quickly from $39

million in 1977 to $570 million, solidifying private equity as an important

asset class with a significant following.

Other regulatory events late in the decade also supported the growth of

the industry, most notably the capital gains tax rate reductions of 1979

(39.875% to 28%) and 1981 (28% to 20%).

Boom and Bust Cycles – a more recent history

The Stars Align.

The First Big Boom (1982 – 1990)

Along with the capital

gains rate tax changes, 1981 saw the peaking of interest rates. Further fuel was thrown on the fire by investment

bank Drexel Burnham Lambert, which essentially created the Junk bond market,

allowing many middle market firms to borrow while bypassing the banks. The issuance of high yield debt climbed from

$1.5 billion in 1982 to $15 billion in 1984 and was almost entirely

underwritten by Drexel. Bank lending as

a percentage of corporate credit fell from just under 60% at the beginning of

the decade, to 15% by its end. Further

spurring the growth of leveraged buyouts was the Tax Reform Act of 1986 which

provided strong incentives for corporations to substitute debt for equity

financing (the curtailment of non-debt tax shields such as the investment tax

credit and depreciation allowances were two such incentives). And, as if this weren’t enough, the stock

market soared. Accordingly, the levered

portion of the private equity industry boomed with commitments climbing nearly

10-fold from $2.4 billion in 1980 to $21.9 billion in 1989. In total, it is estimated that more than 2,000

levered deals with a value in excess of $250 million were consummated. As volume increased, new, niche areas also began

to develop a following including secondary market purchases and

industry-specific funds.

The venture segment

saw numerous new firms enter the market, though capital managed by them grew only

slightly as this area was not buffeted as greatly by the favorable events in

the debt markets. Instead, the segment gradually

went through a shakeout with the best models rising to the top.

It should also be

noted that this decade coincided with the arrival of the “corporate raider” that

used many of the same financing structures as private equity firms, but typically

acted as hostile investors in public companies.

Michael Milken’s bankers at Drexel Burnham supported many of these hostile

investors through the funding of blind pools which enabled the transactions. Levered private equity funds were often

lumped in with the raiders – at least in the public’s eye.

At the time, public

companies being taken private accounted for about ½ of all transaction value

and large mature industries, like retail and manufacturing, made up the bulk of

transactions. Subsequent to the junk bond collapse, these public to private

deals fell to less than 10% of total value and middle market buyouts of

non-publicly traded firms accounted for the bulk of deals (the public to private

relationship currently stands at a more normalized level of approximately 46%

of deal value).

The LBO Bust (1990 – 1992)

As with any

boom, excesses appeared and a number of buyouts fell into bankruptcy, including

those of the Campeau Corporation. Campeau

was a Canadian Real Estate company which acquired Allied and Federated

department stores in the US in the late 1980’s and was one of the first, large

levered bankruptcies of the decade. By

1991, 26 of the 83 large deals completed between 1985 and 1989 had defaulted with

18 entering Chapter 11 bankruptcy proceedings.

LBO volume dropped by over 90% to under $10 billion. At the same time, Drexel Burnham Lambert was

tainted by the charge of insider trading against one of its managing directors,

Dennis Levine. Levine pled guilty and in

turn implicated one of his partners, Ivan Boesky. Boesky in turn, agreed to cooperate with the

SEC regarding his dealings with Michael Milken.

The SEC initiated an investigation of the firm which dragged on for more

than two years with Drexel finally pleading “no contest” to six felonies and

agreeing to pay a fine of $650 million.

During this time, junk bond activity slowed dramatically and funding

declined.

Venture Capital and Technology. The Second Boom (1993 – 2000)

Source:

National Venture Capital Association

Source:

Bain & Company

During the

second boom, both venture capital and levered investments experienced a

re-birth, with the former leading the way.

Private equity commitments overall climbed from roughly $20 billion in

1992 to $240 billion in 2000. Venture

commitments climbed from less than $5 billion to over $100 billion. The overall industry also managed to separate

itself from the taint associated with the 1980’s corporate raiders by

emphasizing the growth and development of acquired companies to the point where

such investors were often welcomed by managements (investments in capital

expenditures and management incentives became more common place during this

time). Risk was moderated as less

leverage was employed in the buyout sector (from 85% - 90% of purchase price in

the 1980’s to 20% to 40% in the 1990’s).

Driving much of the deal activity was the new found interest in the

internet, which drove a frenzy in start-ups and in some cases created new

riches overnight. The vast majority of venture deals were completed in the

Technology Software and Services space, setting the stage for the subsequent

bust.

Source:

National Venture Capital Association

What Goes Up, Must Come Down. The Internet Bubble Bursts (2000 – 2003)

As a large

percentage of the “dot.com” investments were premised solely on the unlimited

potential of the internet rather than a solid business model, many ran into

cash flow issues and the dominoes were set in motion, leading to a large number

of write-offs across technology and telecom-related investments. By mid-2003, private equity fund raising was

at less than half the peak level.

Leveraged buyout firms collapsed with a number of high profile shake-outs

including Hick Muse Tate & Furst and Forstmann Little & Company.

The bust ended

up forcing a greater level of due diligence upon investors and resulted in more

controls being placed on investment partnerships. Bank loans again became a more prevalent form

of deal financing.

Driven by surging

primary market volumes and regulations that increased capital set asides, many banks

and insurers made strategic decisions to exit from in-house private equity

operations. Secondary market transactions

(where one fund buys the private investments of another) grew from under 3% of

commitments to over 5% of the total, joining venture and buyouts as a viable segment

in the private equity world.

Thank You Messrs. Greenspan and Bernanke. The Third Boom (2003 – 2008)

In the aftermath of

the internet bust, seeds were also planted for the industry’s revival. Lower policy rates and a relaxation of

lending standards set the stage for some of the largest private equity transactions

to date. Unlike the boom of the late

1980’s which was fueled by the junk bond market, this boom benefited from the

growth of syndicated bank debt – more than 50% of the LBO’s funded in 2006 were

funded by bank loans. The syndication process

itself resulted in market imbalances which then contributed to the subsequent

bust. First, as the loans did not remain

on the originating bank’s books, there was the likelihood that the diligence

conducted in making the loans was relaxed. Second, a

number of the deals were funded with debt that had weak covenants

(“cov-lite”). Further, regulatory

changes (the imposition of Sarbanes Oxley), helped the buyout industry convince

public companies that life as a private firm might be preferable while the same

legislation hurt the IPO dreams of many venture firms. As a result, more of the venture deals ended

up being done with strategic buyers (a purchaser in the same industry as the

company) and secondary volumes grew, comprising over 20% of total transaction

value. The “Greenspan Put”, as it came

to be known, convinced industry players and investors that the environment

would not change and overall risk taking appetite increased. Funding volume hit a peak of just under $700

billion in both 2007 & 2008.

Source:

Bain & Company

A Different Kind of Exit

Toward the end

of the third boom, an exit of sorts was seen by some of the larger private

equity firms, though not in the usual context of selling portfolio firms. In 2007 the Blackstone group filed for an IPO with the SEC and proceeded

with a sale to the public (12.3% stake).

In the same year, the Carlyle Group also sold an interest in the

management company (7.5% interest). In

January of 2008, Silver Lake Partners followed suit with a 9.9% sale of its

management company to CalPERS. To the

cynical, this might seem like a backdoor way to raise liquidity for partners at

a time when the size of their investments limited strategic sales and when the

weakening market environment limited the IPO door. It was promoted by the sellers as a way to

spread the riches of private equity to a wider audience of investors.

Yet Another Bubble Bursts

Low interest

rates, no-money down mortgages and new residential mortgage financing vehicles

led to an unprecedented run in the US housing market from the early part of the

decade and into 2007. As this bubble

inevitably burst, its repercussions were felt world-wide. From the failure of a Bear Stearns hedge fund

during the summer of 2007 to the failure of Lehman Brothers a year later, the

credit markets froze and spreads widened to record levels. Globally, stock markets fell by more than 40%

and as might be expected, the leveraged finance markets came to a standstill,

with deal activity troughing at $134 billion in 2008. Only the Distressed and Turnaround funds saw notable

increases in fund raising in 2007 and 2008.

Source:

Probitas Partners

A Slow and Steady Recovery

It wasn’t until after

more than a year of unprecedented intervention by US and other western central banks

that confidence was secured and funding activity picked up. From a trough of $296 billion in 2010, funding

rose slowly to reach $461 billion in 2013 (2014 activity through August is on a

similar pace).

Source:

Bain & Company

The Present

The private

equity industry is led by buyout strategies which comprised 37% of the capital

raised last year. Tangible asset

strategies (Real Estate, Infrastructure and Natural Resources) made up an

additional 31% of the total, while distressed, venture capital and other

strategies comprised the remaining commitments.

Source:

Preqin Global Private Equity Report 2014

The Future

While nothing is

ever certain, the history of private equity has shown how the industry attempts

to take advantage of (or is effected by) the tax, regulatory, interest rate and

stock market environments. Given our

reading of the tea leaves, we think the following factors will drive and shape

the industry in the decade ahead:

- Increased regulatory and operational

scrutiny

- Diminished interest in hedge funds

- Greater demand for private equity in

the alternatives space

- A battle between mega-firms and

smaller, boutique style managers for investor monies

- A headwind for buyout and other private

equity strategies employing leverage

Increased regulatory and operational scrutiny

is a near certainty. Following on the heels

of the financial crisis, investors have stretched in search of new

opportunities as interest rates and spreads fell to historic lows. Perhaps because of this, alternative asset

categories have become more prevalent and regulators, accordingly, don’t want

to drop the ball again. The following

areas will be under watch in the private equity realm:

- Expense allocation between the funds

of a given manager

- The asset valuation policies of these

funds

- The co-investment policies of the

manager

- Fee transparency

- Form PF and marketing material scrutiny

- An increased push by investors to

outsource (and upgrade) manager operational capabilities

On balance, increased

scrutiny should bode well for the growth of the industry. While it will increase the costs of doing

business, greater oversight will also allow investors not currently in the

segment to feel more comfortable about future commitments. At the same time, many service firms

specializing in providing non-investment services such as Fund Administration

and Compliance Outsourcing will help limit smaller managers’ cost increases

while providing them with best in class services.

A diminished interest in Hedge Funds

is quite possible. Following a number of

years of less than stellar results and a well-publicized decision by CalPERS,

the largest public fund in the United States, and PFZW, the $150 billion Dutch Healthcare system, to divest from the category, we put

a high probability on the following:

- The potential for “follow on” moves

(away from hedge funds) by smaller plan sponsors

- A move away from the higher

expenses associated with fund of fund programs and toward direct placement by

those committed to the category, a continuation of a trend that is already

underway

- An opportunity for other

alternative categories such as Private Equity to gain share

The fact that we are likely to be in a low return

environment for traditional asset classes (see our

white paper, “Forecasting Return

Expectations”) and investors have already taken on more risk in the quest

for return, means many are now more likely

to consider investing in what may be “new” asset classes to them. With private equity allocations across large

plans currently at 7% of assets, there is still room for the segment to gain

share. Also, given the generally

fulfilled return expectations to date, private equity would seem to be a

natural fit for many.

Source:

Bain & Company, Cambridge Associates

However, within the industry, where investors focus is

still up in the air.

We are currently seeing different behaviors by investors in terms of the

size of manager with whom they have comfort.

- The State of Wisconsin as well as Colorado

Fire & Police have explicitly announced an intention to invest more with

smaller managers where they feel interests are better aligned and where more opportunity to add alpha is possible

- Los Angeles County ERS is also “looking

at smaller managers”

- CalPERS and the State of Michigan have

already increased allocations with mega-firms citing the ease of oversight when

managing large pools of capital

Ultimately,

performance will likely determine which preference becomes dominant, though

both are likely to co-exist for the near term.

Finally, given today’s

historically low level of interest rates and credit spreads, along with the

increased use of leverage in recent transactions, it will be more difficult for strategies dependent upon leverage to do

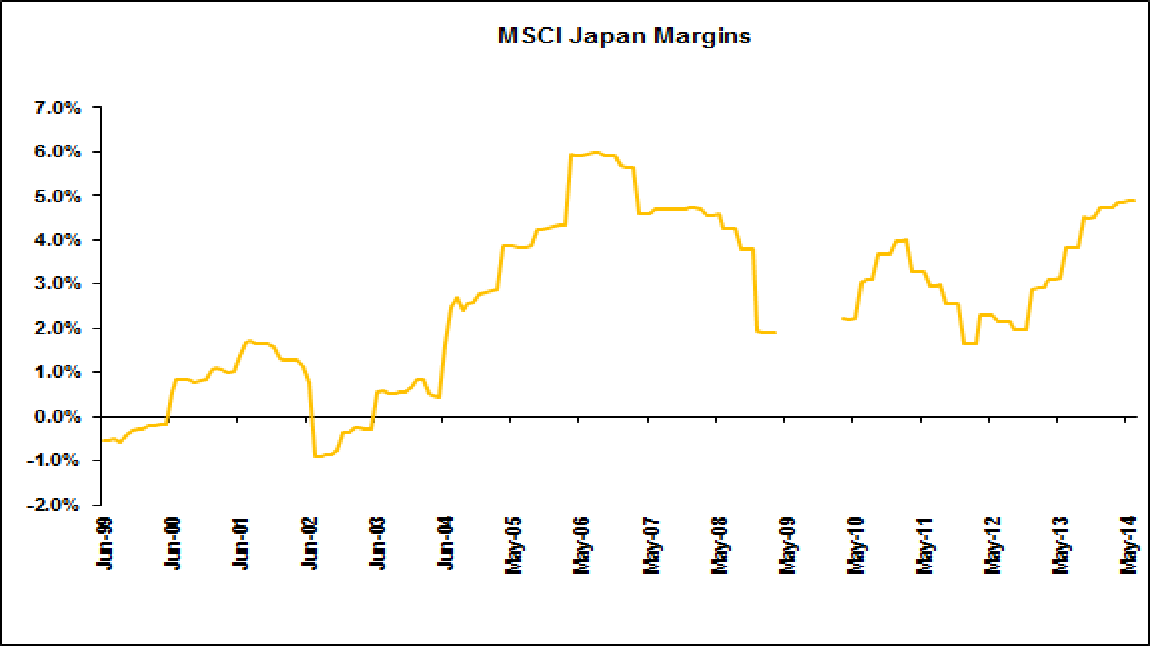

as well in the future as they have in the recent past. In fact valuation levels are approaching the

last cycle’s peak.

Source:

Bain & Company, S&P Capital IQ

Conclusion

At the end of

the day the future looks bright for most areas within the private equity

space. Investors are underweight the

asset class, private equity has historically met investor expectations and it is

looked upon favorably by current investors.

With a low return environment for traditional asset classes a high

probability, new sources of return will continue to be sought by plan sponsors. Private equity has every reason to be high on

most lists.